Buyer-Side Mortgage Deposit Support?

Will the Government bring in targeted Buyer Side support measures, for first time buyers and lower income households?

It's a simple statement but an important one: for builders to build, there must be buyers to buy. Greater support for buyers is needed to boost housebuilding and it is vital to see new buyer support measures in the Budget.

In spite of lower interest rates, home buying remains sluggish. Many housebuilders are having to sell to rental landlords at bulk discounts to counter the current market headwinds. In turn, this reduces housebuilder profits and affects investment decisions in opening new sites, contributing to lower housebuilding activity overall. It also means more renting and less home ownership.

A healthy housing market is one with a healthy proportion of home buyers. There are a range of measures that could support increased new homes buyer activity. The priority must be a new type of buyer support scheme for newly built homes.

HM Treasury is understood to be keen on see greater opportunity for home ownership, particularly for those on lower incomes as well as wanting to see house building numbers grow. Home ownership is an expressed priority of the Prime Minister. This will be a key area to watch in the Budget.

At the Housing & Finance Institute, we have recommended that the following buyer support measures should be considered:

- Pension deposit flex: allowing pension scheme flexibility to help young people save for their first deposit. For example through a pension diversion scheme that would allow workers to opt to pay their pension contribution and employer top up into a savings ISA for up to 5 years. This could unlock significant deposit savings for younger workers, with anything over and above the deposit required for their new home going back (tax free) into their pension pot.

- LISA: reviewing and updating the Lifetime ISA. The LISA (and its predecessor Help to Buy ISA) is a hugely successful savings scheme to support buyers to save for a home deposit. There were over 1.3 million accounts in 2023/24. However, it is not suited to every regional market or every saver, and needs updating to support home buyers in the years to come, particularly in London and parts of the South East.

- Equity Loans: bringing in targeted equity loan schemes for those buyers of new homes who are on lower and middle incomes.

- Alternatives to shared ownership schemes: There is scope for new discounted and deferred purchase schemes to offer an alternative to shared ownership.

As noted above, previous Help to Buy schemes stimulated growth with a peak expansion rate of over 15% in 2014 and 2016. Targeted buyer support intervention remains the surest way to get building rates back on track towards the 1.5million homes target - and boost national economic growth too.

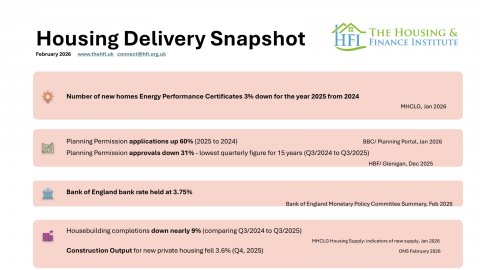

February 2026 Housing Delivery Snapshot

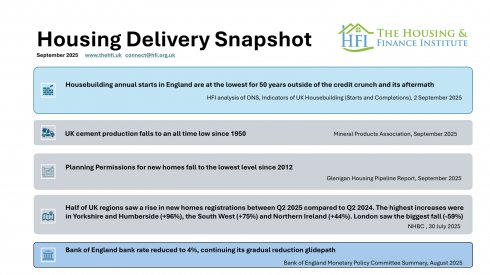

September 2025 Housing Delivery Snapshot

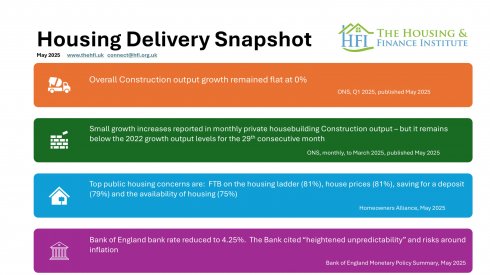

May 2025 Housing Delivery Snapshot

March 2025 Housing Delivery Snapshot

January 2025 Housing Delivery Snapshot

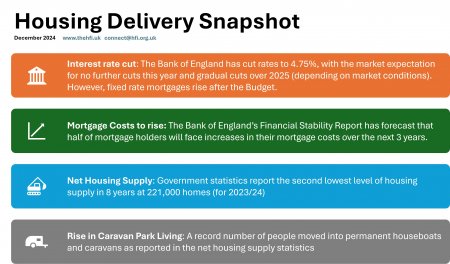

December 2024