08 SEP 2024

A Fairer Right to Buy ?

A Fairer Right to Buy ?

The Government has indicated that it intends to reform the Right to Buy (RTB).

This is a welcome move. RTB reform was recommended by the Housing & Finance Institute in the HFI Budget for Housing in March 2024. This is because the existing operation of the RTB system acts as a blocker for the building of new council homes and is considered to create an unfair windfall for people who have been social housing tenants for as little as 3 years.

The Government has indicated that it will look to reduce discounts on the sale of council houses and increase the number of years before tenants qualify for a substantial discount.

Here we look at the options and alternatives to RTB that the Government could consider. These are as follows:

- Reduce the RTB discount levels Increase the number of qualifying years

- Cap the discount to the amount of rent paid

- Exclude new developments from RTB

- Introduce a new Right to Buy Deposit scheme for social tenants

- Create a new national lower income transferable deposit scheme available to all social and private renters

Background

Council tenants have been able to buy their council homes since the 1936 Housing Act. The 1980 Housing Act greatly extended the policy and has provided a ladder to home ownership for millions of Britons. Over the years the application of the policy, the number of qualifying years, percentages and caps have been changed from time to time. This is sometimes to encourage the use of RTB and sometimes to restrict it. Currently, the qualifying period for RTB is three years for a social housing tenant to get a discount of 35% of the value of the social home.

In terms of the value of the RTB discount, Right to Buy has moved away from its original roots in property costs and the value of rent paid, to the current percentage discount scheme. This is estimated (LGA/Savills/ ARCH/NFA) to be an additional giveaway of value over and above rent paid of up to £2billion since 2012. To put this in context, it is equivalent to 10,000 additional replacement RTB homes over the last decade. The operation of the percentage discount scheme in providing an unfair windfall is explained by the research analysis as follows:

"The minimum discount applying against current values is simply a "broken" concept when comparing to rent paid: This is exemplified in the example below: a property worth the national average (outside London) of £138,000 with a tenant occupying a property for three years has paid rent (at the national average of c£85/week outside London) of £13,260 whereas the minimum discount for a house is 35% after 3 years, or around £48,000."

It is therefore clear that there can be a large windfall for newer social housing tenants. This is particularly problematic given that the financial arrangements entered into by councils to finance new housing may be around 20 years and can often be much longer than that.

This means that because of the way social and affordable housing is financed, the current discount policy acts as a disincentive for to build new social and affordable housing. It might be thought that different thinking applies in the case of older housing stock – given that this older stock has served an economic value to social housing and should have been paid down. However, it is often the case that older housing stock requires additional investment to be brought to decent homes and appropriate environmental standards. It is important that such investment is taken into account in the application of the RTB programme.

Options for Reform

Given that the Government has indicated that it will look to reduce discounts and increase the number of qualifying years there are a number of ways in which such reforms could be implemented.

Rebalancing discounts and qualifying years: An immediate reform, set out in HFI's Budget for Housing, is that the Right to Buy discount could be capped at the value of the rent paid. Only after 10 years would the rent cap be disapplied so that the RTB discount would be awarded without reference to a rent cap. That would mean that long-term tenants would continue to benefit from the full discount rate.

Right to Buy Deposit Scheme: As regards new build social housing, because the financing is so long term, an option may be to change the Right to Buy discount to a Right to Buy Deposit scheme so that social tenants will have the deposit they need to purchase another property and own a home of their own. Such a reform would support local authorities to build more social and affordable housing and make the most efficient and productive use of the overall affordable housing stock.

Lower-income renters deposit scheme: The relative decline in the overall proportion of social and council housing since its heyday, when around one-third of households lived in council housing, has caused a big demographic change. Many more people on lower incomes are now in private rent, as opposed to social rent, accommodation. Given this, additional support to home ownership for lower-income households is now required. For example, a new national deposit scheme which supports lower-income households into home ownership, whether from private rented accommodation or social/council homes could make a huge difference to helping lower income households onto the housing ladder.

As the HFI has long argued, reform to Right to Buy is overdue. This is an important opportunity for Right to Buy to operate more fairly to all, support councils in building new council housing and introduce additional measures to support lower-income renters into home ownership .

Further Reading:

LGA/ Association of Retained Council Housing/National Federation of ALMOs: Research into the Right to Buy within the Housing Revenue Account (January 2023)

Government HRA resources: Housing Revenue Account (HMG website)

HFI: A Budget for Housing (March, 2024)

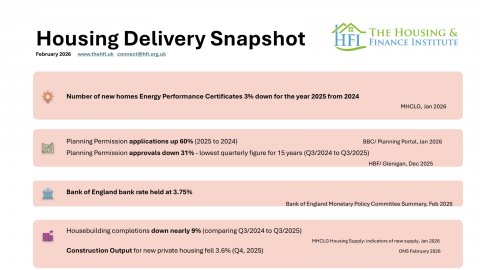

February 2026 Housing Delivery Snapshot

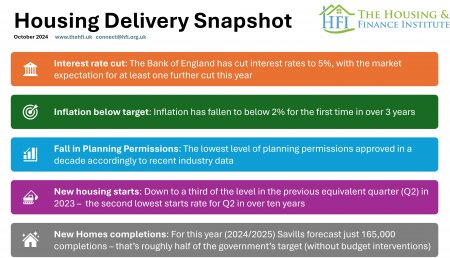

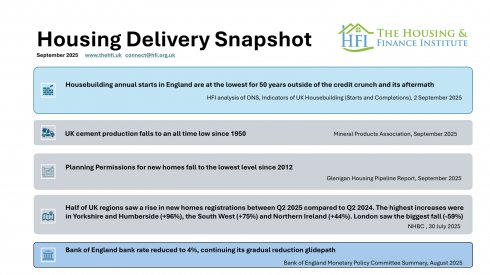

September 2025 Housing Delivery Snapshot

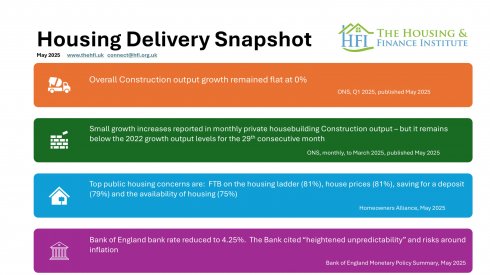

May 2025 Housing Delivery Snapshot

March 2025 Housing Delivery Snapshot

January 2025 Housing Delivery Snapshot

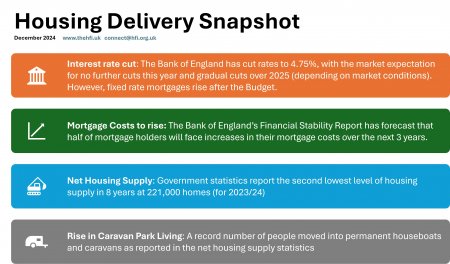

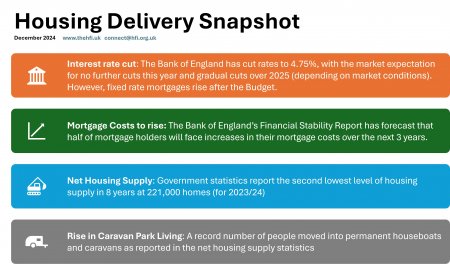

December 2024