Helping First Time Buyers in a Budget for Housing March 2024

Let first-time buyers use pension contributions to fund mortgage deposit – Chancellor urged

First-time buyers should be allowed to use contributions from their private pensions for mortgage deposits, according to a radical new report urging the Chancellor to deliver a "Budget for Housing".

The Report also calls on the Chancellor to introduce new government backed housing deposit guarantees, and housing deposit loans which would be repayable through the tax system in the same way as student loans.

The plan from the cross-party Housing and Finance Institute (HFI) is intended to kick-start the sluggish housing market and bring home ownership within the reach of tens of thousands of under-40s currently priced out of the market.

The average age of a first-time buyer is now 33 in England and has been steadily creeping up for years under the impact of rising house prices – it was as low as 29 in the 1990s.

The average price for a first-time buyer's home stands at around £225,000 across the UK. That means that by the time people are in their late 20s or early 30s many could have enough set aside by transferring pension contributions to cover a typical deposit of between 5% and 10% (between £11,250 to £22,500). A government housing guarantee or housing loan scheme would clearly provide a much faster route onto the housing ladder.

The HFI estimate that the pension transfer and new government loan schemes recommended in the report could help get housing back on track – meaning an extra 30,000 more homes and homeowners a year. That would be 30,000 more people able to get onto the first rung of the housing ladder every year.

In a 12-point plan submitted to Jeremy Hunt ahead of his March 6 Budget, the HFI additionally calls for the building of 100,000 new affordable homes, arguing that the government and local councils stand to save over £3 billion a year while boosting the economy by £15 billion. The Institute argues that the cost of building the new homes would be heavily offset by reductions in the housing benefit bill which costs over £20billion each year. Reducing discounts on 'right to buy' deals would also help to fund the 100,000-unit HFi 'homemaker' affordable housing scheme.

Further measures in the Report includes a plan to ease pressure on the greenbelt by building on disused 'brownbelt' land. These are islands of brownfield land inside the greenbelt, such as a disused airfield or factory, which should be made automatically available for redevelopment into housing.

Sir Steve Bullock, chair of the HFI said urgent action is needed to tackle the housing crisis. "From homelessness and affordable housing to home ownership and house building, the housing crisis is getting worse.

"The measures in this report are practical steps that can be taken in the Budget to end the housing crisis. That includes building more homes, including on disused brownbelt land, and rewarding councils that deliver the homes we need."

MP Natalie Elphicke, head of housing delivery at the HFI, called on the Chancellor to deliver a 'Budget for Housing'.

"Help for first-time buyers to raise a mortgage deposit must be a key priority in this budget. Government housing deposit loans and a pension transfer scheme would help kickstart the sluggish housing market and bring home ownership back within reach of tens of thousands of under 40s currently priced out of the market.

"Building 100,000 new affordable homes would save the taxpayer over £3 billion a year and boost the economy by £15billion.

"There is no excuse for inaction on delivering the homes that are needed. Now is the time to back first-time buyers and get Britain building again."

Access the HFI Report here: Budget for Housing 2024 Report

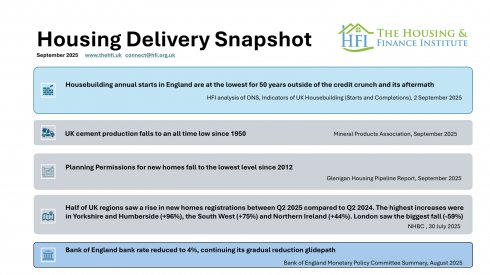

September 2025 Housing Delivery Snapshot

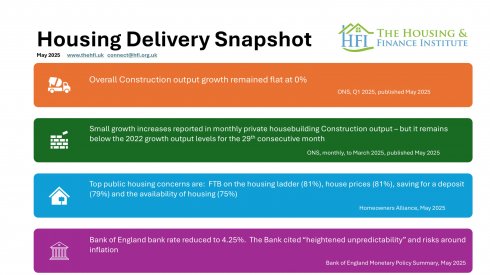

May 2025 Housing Delivery Snapshot

March 2025 Housing Delivery Snapshot

January 2025 Housing Delivery Snapshot

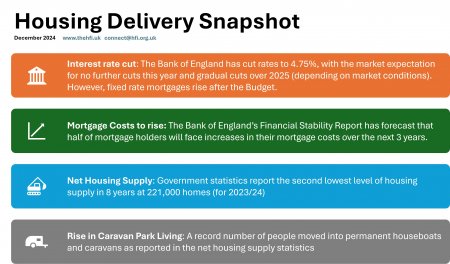

December 2024