04 OCT 2017

Reducing the Hurdles to Home Ownership for the Young

Photograph credit: Rahil Ahmad and the Legatum Institute

Photograph credit: Rahil Ahmad and the Legatum Institute

At Conservative Party Conference 2017, the HFI took part in an event hosted by ConservativeHome in partnership with the Legatum Institute entitled 'The country we want to be: pathways to prosperity'.

The session included contributions from Rt Hon Sajid Javid MP, Secretary of State for Communities; Matthew Elliott, Senior Fellow, Legatum Institute; Nicholas Boys-Smith, CEO, Create Streets; Lewis Sidnick, Head of Corporate Affairs, NHBC; Danny Kruger, Senior Fellow, Legatum Institute; Natalie Elphicke, Housing & Finance Institute; and Baroness Philippa Stroud, CEO of Legatum (Chair).

The context of the session was the Legatum Institute's latest paper – 'Public opinion in the post-Brexit era: Economic attitudes in modern Britain' that included evidence of heightened public attitudinal importance attached to housing and Legatum's current 'More Good Homes' project.

Earlier at the conference the Government announced a £10billion extension to the Help to Buy Equity Loan scheme had been announced and the session included discussions around the decline in home ownership, particularly for young people.

The Help to Buy Equity Loan Scheme: Background

The National Audit Office provides useful commentary on the policy context and timing of the Help to Buy Equity scheme as follows:

"1. The Department for Communities and Local Government (the Department) published its housing strategy, Laying the Foundations, in November 2011. In it, the government set out what it sees as the three main barriers to home ownership:

- Potential home owners cannot afford mortgage finance.

- Lenders restrict access to mortgages to buyers with big deposits.

- Developers do not build enough new homes, partly because potential buyers cannot raise a mortgage.

2. The government announced the Help to Buy scheme (the scheme) on 20 March 2013 as one of several measures to address these barriers and support the housing market. It opened the scheme to the public 12 days later, on 1 April 2013. The scheme's objectives are to turn the desire for home ownership into demand for new homes, by improving the affordability of, and access to, mortgage finance and to encourage developers to build more new homes."

Help to Buy has shored up activity by housebuilders since the credit crunch and has created 320,000 additional home owners. It has also underpinned an increase in housebuilding and has resulted around 190,000 net new homes last year, the 3rd highest outturn in the last 15 years. 2016/17 was the 5th highest year of housebuilding in more than quarter of a century. Help to Buy has had a strong part to play in the improving performance of the housing markets.

Decline in Home Ownership for younger people

However, the steps taken to date haven't reversed the home ownership deficit for younger people. That remains a stark political and economic problem.

Home ownership remains at historically low levels. Britain is fast becoming a nation of renters. Moreover, the headline figures mask serious changes in home ownership opportunity for younger people. Since 2001, home ownership has nearly halved for the under 35 age group. This was confirmed by new research released today, showing that homeownership for the under 35 age group has fallen by 21% over the last quarter alone.

However, getting younger people on to the housing ladder is not just a building challenge – it is a financial and political challenge also. There is a need to provide greater choice for young people so they can decide when they want to rent and when to own and provide ladders to security and financial stability that previous generations have enjoyed.

Beyond Help to Buy - A fresh policy approach?

At the event, recognising the success of Help to Buy, Natalie asked whether it was also timely to consider whether additional targeted support for young people may be appropriate in order to lower the hurdles for younger people to access home ownership, should they want to own their own home. Such targeted support might include:

Stamp Duty Reform: Stamp duty exemptions for first time buyers are regular policy sticking plasters. It may be that the time has come for a more extensive review of stamp duty. Making stamp duty payable on sales rather than purchase would lower the hurdle for young people. It could also free the ladder at the other end, helping older people with downsizing.

Direct Home Deposit Loans: Help to Buy Equity Loans provide 20% by government loan and requires a 5% deposit by the home purchaser. However, there are now a number of mortgage products that require a much lower equity stake than 25%. A direct loan by government of up to 10% per property could double the number of people that can be helped. A home deposit loan could be recovered through the tax system from deductions and could allow a difference between repayment trigger dates and amounts for higher and lower paid salaries, and/or deferring final repayment to the sale of the property.

Housing Allowance Deductions At Source: A housing allowance tax scheme could be introduced where young home owners' mortgage interest can be deducted from tax. For young working renters, an innovative approach would be to have some housing tax rebates referenced to rental payments where the rebate of tax was paid directly into a housing ISA to contribute to a home deposit savings scheme.

Britain is building many more homes but not necessarily increasing the choice to own a home, particularly for young people. To give the choice of home ownership to a new generation, additional or different policy interventions may be needed.

Further Information

NAO Information: https://www.nao.org.uk/wp-content/uploads/2015/03/The-Help-to-Buy-equity-loan-scheme.pdf

The Legatum Research: http://www.li.com/activities/publications/public-opinion-in-the-post-brexit-era-economic-attitudes-in-modern-britain

DCLG Statistics on net additional housing: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/568412/LiveTable_122.xls

DCLG Statistics on housebuilding: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/639717/LiveTable208.xlsx

Announcement of Help to Buy extension: http://www.bbc.co.uk/news/business-41459446

Government release on progress of Help to Buy to date: https://www.gov.uk/government/news/help-to-buy-supports-over-320000-people-in-buying-their-own-home

Telegraph article on decline in young home owners: http://www.telegraph.co.uk/property/house-prices/number-homebuyers-aged-18-35-drops-21pc-millennials-continue/amp/

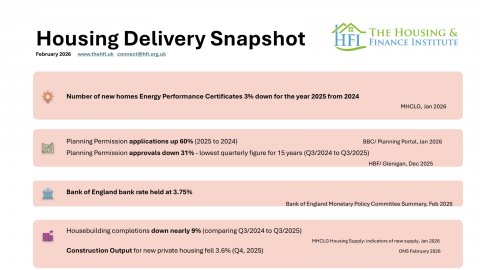

February 2026 Housing Delivery Snapshot

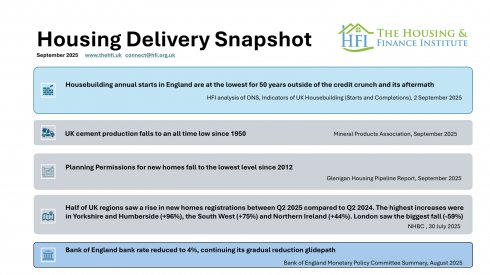

September 2025 Housing Delivery Snapshot

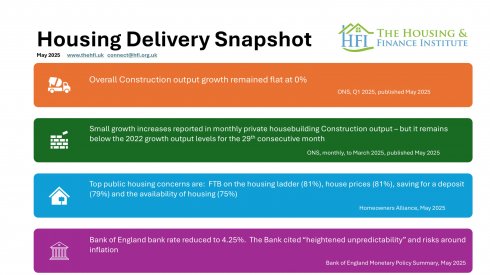

May 2025 Housing Delivery Snapshot

March 2025 Housing Delivery Snapshot

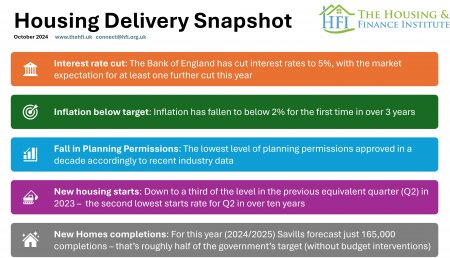

January 2025 Housing Delivery Snapshot

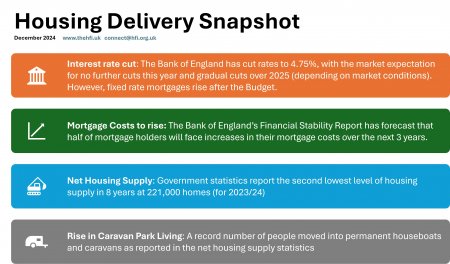

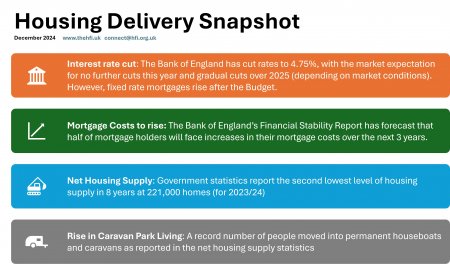

December 2024